As more businesses begin accepting and holding cryptocurrency, the accounting implications are becoming increasingly important — and often misunderstood. Crypto offers exciting opportunities, but it also comes with specific rules for recognition, valuation, and reporting.

If your business is using crypto, for instance, Bitcoin, in any way — holding them, receiving them from customers, or using them to pay vendors — it’s essential to understand how each action affects your financial statements. Proper treatment protects your business from surprises at year-end and ensures clean, compliant books.

Below is a straightforward guide to help you navigate the core accounting principles every business owner should know.

1. Holding Crypto on Your Balance Sheet

When your business owns cryptocurrency, it is treated as a non-cash digital asset.

You record it at its fair market value on the day you acquire it, using the following entry:

- Debit: Digital Asset (Asset)

- Credit: Cash / Payable / Revenue (depending on how it was acquired)

This initial value becomes your cost basis.

Any time you:

- sell,

- convert,

- or use that crypto,

you must calculate the gain or loss based on how the market price has changed since acquisition.

- If the value has increased → you recognize a gain

- If the value has decreased → you recognize a loss

These gains and losses flow through your income statement.

2. Receiving Crypto as Payment From Customers

Receiving crypto from a customer works the same as receiving property.

Revenue is recognized at the fair market value of the crypto on the date you received it — based on a reliable exchange price. That amount becomes the cost basis of the crypto you now hold.

Later, if you convert or spend that crypto, you must recognize another gain or loss, depending on how the price has changed since receipt.

This means two things happen:

- Revenue is recognized once — at the time earned.

- Gain or loss is recognized later — when the crypto is sold or used.

Understanding this timing is essential for accurate financial reporting.

3. Paying Vendors Using Crypto

Paying a vendor with crypto triggers two separate accounting steps:

Step 1: Recognize the gain or loss

You must calculate the difference between:

- the crypto’s current fair market value, and

- your cost basis.

Step 2: Record the expense

Then you record the vendor expense at the fair market value at the time of payment.

Example:

You purchased Bitcoin at $30,000.

You pay a vendor when Bitcoin is worth $36,000.

- You recognize a $6,000 gain.

- You record the vendor expense at $36,000.

This is the area where many businesses get surprised — especially at tax time.

4. Internal Controls Your Business Needs

Because crypto values fluctuate quickly, accurate recordkeeping is essential.

You should track:

- Date acquired

- Amount acquired

- Cost basis

- Date disposed

- Market value at disposal

- Vendor/customer tied to the transaction

- Pricing source used

Use reputable pricing data and apply the same valuation source consistently across all transactions.

Strong internal controls reduce errors and help prevent misstatements on your financials.

5. Practical Recommendations for Clean, Accurate Crypto Accounting

To keep your books organized and prevent year-end issues, consider the following best practices:

- Maintain a dedicated crypto asset register (similar to fixed asset tracking).

- Use a wallet dedicated exclusively to the business.

- Avoid mixing personal and business crypto holdings.

- Reconcile crypto activity monthly, not once per year.

- Work with an accountant or tax professional experienced in crypto cost basis rules

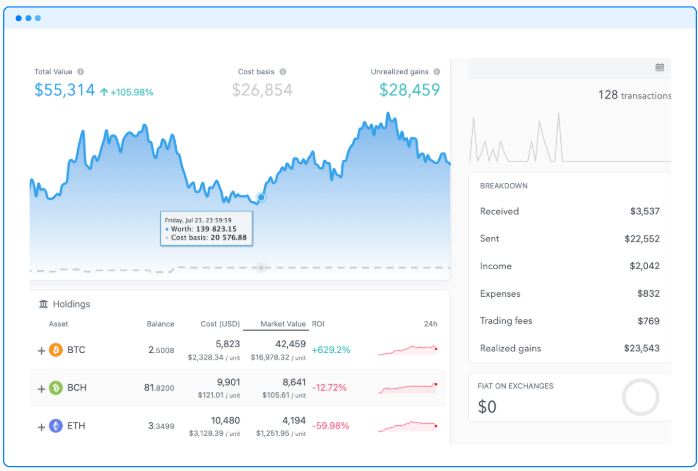

- Consider a software like Koinly to track your income, expense and gains/losses. See an examplye below

Proper accounting ensures your reporting is accurate and eliminates surprises when it’s time to file taxes or prepare financial statements.

Bringing Clarity to a Complex Area

Crypto is here to stay — and businesses that engage with it need sound processes, clear documentation, and reliable reporting. With the right approach, you can confidently integrate crypto into your operations while maintaining accuracy and compliance.

If you need help reviewing your crypto transactions, establishing internal controls, or creating a clean reporting process, our team is here to help.

Contact us today to learn how we can support your business:

https://flemingandassoc.com/contact/